Gaza War Extends Toll on Israel’s Economy

By: Alexander Kozul-Wright

Last week, Fitch Ratings downgraded Israel’s credit score from A+ to A. Fitch cited the continued war in Gaza and heightened geopolitical risks as key drivers. The agency also kept Israel’s outlook as “negative”, meaning a further downgrade is possible.

After Hamas’s deadly attack on October 7 2023, Israel’s stock market and currency nosedived. Both have since bounced back. But concerns about the country’s economy persist. Earlier this year, Moody’s and S&P also cut their credit ratings for Israel.

So far, Israel’s war on Gaza has killed more than 40,000 Palestinians and decimated the economy in the besieged Palestinian enclave.

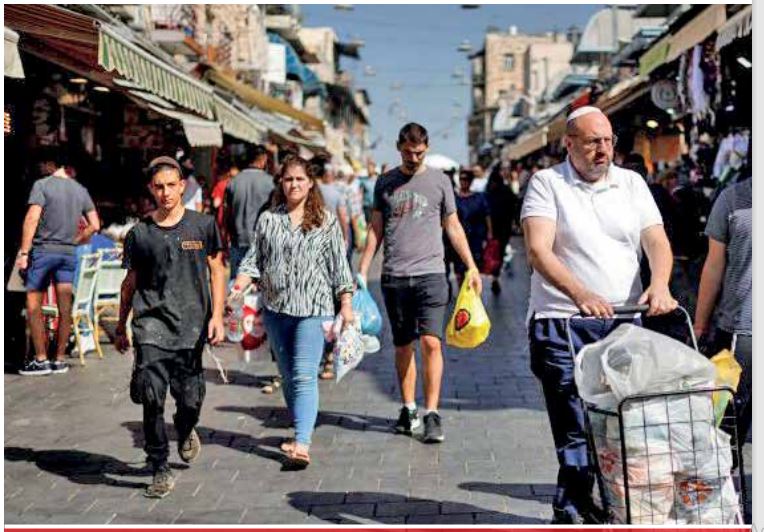

There are signs of a blowback in Israel, too, where consumption, trade and investment have all been curtailed.

Separately, Fitch warned that heightened tensions between Israel and Iran could incur “significant additional military spending” for Israel.

The Bank of Israel has estimated that war-related costs for 2023-2025 could amount to $55.6bn. These funds will likely be secured through a combination of higher borrowing and budget cuts.

The upshot is that combat operations are putting a strain on the economy. On Sunday, Israel’s Central Bureau of Statistics estimated that output grew by 2.5 percent (at an annual rate) in the first half of 2024, down from 4.5 percent in the same period last year.

Other parts of the economy have taken a significant hit. In the final quarter of last year and in the weeks after the war began, Israel’s gross domestic product (GDP) shrank by 20.7 percent (in annual terms). The slump was driven by a 27 percent drop in private consumption, a drop in exports and a slash in investment by businesses. Household expenditure snapped back at the start of the year, but has since cooled.

Israel also imposed strict controls on the movement of Palestinian workers, forgoing up to 160,000 workers. To tackle those shortages, Israel has been running recruitment drives in India and Sri Lanka with mixed results. But labour markets remain undersupplied, particularly in the construction and agriculture sectors.

According to the business survey company CofaceBDI, roughly 60,000 Israeli companies will close this year due to manpower shortages, logistics disruptions and subdued business sentiment. Investment plans have, in turn, been delayed.

At the same time, tourist arrivals continue to fall short of pre-October levels.

Meanwhile, the war has triggered a steep rise in government spending. According to Elliot Garside, a Middle East analyst at Oxford Economics, there was a 93 percent increase in military expenditure in the last three months of 2023, compared to the same period in 2022.

“In 2024, monthly data suggests military expenditure will be around double the previous year,” Garside said. Much of that increase will be used on reservist wages, artillery, and interceptors for Israel’s Iron Dome defence system.

Garside said these expenditures “have mostly been financed by issuance of domestic debt”.

Israel has also received some $14.5bn supplemental funding from the United States this year, on top of the $3bn in annual aid that the US provides to the country.

Garside noted, “We are yet to see any major cutbacks to other parts of the budget [like healthcare and education], although it is likely that cuts will be made in the aftermath of the conflict.”

Absent a full-scale regional war, Oxford Economics anticipates that Israel’s economy will slow to 1.5 percent growth this year. Subdued growth and elevated deficits will put further pressure on Israel’s debt profile, which will likely raise borrowing costs and soften investor confidence.

Fitch expects Israel to permanently increase military spending by 1.5 percent of GDP compared to prewar levels, with unavoidable consequences for the public deficit. Last week’s rating report noted that “debt [will] remain above 70 percent of GDP in the medium-term”.

The report emphasised that public finances have been hit, and that “we project a deficit of 7.8 percent of GDP in 2024 [up from 4.1 percent last year]”. Israel’s far-right Finance Minister Bezalel Smotrich has publicly disagreed, and expressed confidence that it will fall back to 6.6 percent this year.

“The downgrade following the war and the geopolitical risks it creates is natural,” Smotrich said, according to media reports. He added that a responsible budget will soon be passed, and that Israel’s ratings would rise “very quickly”. For now, doubts remain about the budget’s timeline.

There has been speculation that Prime Minister Benjamin Netanyahu is delaying his fiscal package, which may prove domestically unpopular. Failure to pass a budget by March 31, 2025 would automatically trigger snap elections.

Earlier mid of August month, Israel’s Central Bank chief – Amir Yaron – called on Netanyahu to speed up the 2025 state budget, as further delays risk stoking financial market instability.

For its part, Fitch believes that Israel will adopt a combination of austerity measures and tax hikes. But in their August 12 report, Fitch analysts Cedric Julien Berry and Jose Mantero pointed out that “political fractiousness, coalition politics, and military imperatives could hinder [fiscal] consolidation”.

What’s more, the rating agency warned that “the conflict in Gaza could last well into 2025 and there are risks of it broadening to other fronts”.

On 19 August 2024, US Secretary of State Antony Blinken said that Netanyahu had accepted a “bridging proposal” designed to reach a ceasefire between Israel and Hamas and diffuse growing tensions with Iran.

The following day, eight Palestinians were killed in an Israeli attack on a crowded market in Deir el-Balah, in central Gaza.

Hamas has yet to agree the bridging proposal, calling it an attempt by the US to buy time “for Israel to continue its genocide”. Instead, the Palestinian group has urged a return to a previous announced by US President Joe Biden, which has more guarantees that a ceasefire would bring about a permanent end to the war.

Netanyahu has insisted that the war will continue until Hamas is totally destroyed, even if a deal is agreed. Israeli officials, including Defence Minister Yoav Gallant, have rubbished the idea of a total victory against Hamas.

A decades-old shadow war between Israel and Iran surfaced in April, when Tehran launched hundreds of drones and missiles at Israel in response to the Killing of two commanders from Iran’s Islamic Revolutionary Guard Corps (IRGC) in Damascus.

Along its Lebanese border, Israel has traded near-daily attacks with Hezbollah since last October. The armed group began firing on Israel as a show of solidarity with Hamas. Both organisations have close ties with Iran.

More recently, the assassinations of Hamas leader Ismail Haniyeh in Tehran and Hezbollah military commander Fuad Shukr in Beirut have sparked fears that the conflict in Gaza could metastasise into a regional conflict.

“The human toll [of a wider war] could be significant. There would also be huge economic costs,” says Omer Moav, an Israeli economics professor at the University of Warwick.

“For Israel, a long war would come with high costs and greater deficits,” he said.

In addition to undermining Israel’s debt profile, Moav said that prolonged fighting would incur “other costs”, like labour shortages and infrastructure damage, as well as the possibility of international sanctions against Israel.

“Israel is currently ignoring the fact that economics may lead to greater [societal] damage than war itself,” said Moav. “The government is not behaving responsibly. Does it want to avoid the costs of war, or does continued conflict serve political interests?”

{kind=link}